Debt Creates Money, Where Does it Go? Part 1

Debt Creates Money, Where Does it Go? Part 1

How and why most of the world’s economies are founded in debt

January 18, 2021

Estimated read time: 10 minutes

Why is Money Created Through Debt?

Option 1: No Money is Created

Option 2: Money is Actively Printed

Option 3: Money is Created Through Debt

How is Money Created Through Debt?

Commercial Banks

The Federal Reserve

Epilogue

Why is Money Created Through Debt?

In the 2008 housing crisis, nearly 10 million people lost their homes because the interest on their mortgage multiplied overnight. Many financial gurus and media outlets actively condemn debt while some religions actively forbid any interest paying loans.

For many people, their experience with debt is, at best, something that erases personal wealth and, at worst, something that has ruined their lives. So when somebody says “debt creates money” an understandable reaction is to respond with derision if not outright anger.

But when you get a paycheck, that money comes from a business. When a business makes money, it comes from a customer. If customers and businesses just passed the same money back and forth, then how would new businesses get created? How would new people, our growing population, find jobs?

There are three options:

Option 1: No Money is Created

Let’s say we lived in a world wherein we had mined all of the Earth’s gold and the dollar had a fixed conversion rate to gold. In this system there would be a fixed amount of money but an increasing amount of people. The only way for everyone to have an income in such a situation is for the value of a dollar to increase.

Think about it like this. Assume a closed society where there are 10 total people, $100 in total, and bread costs $10 to purchase. In this environment, everyone has to possess $10 whenever they’re hungry or else somebody starves. One year later the population grows to 20 people, but there’s still only $100 total. If bread still costs $10 then not everyone can afford bread. The only way it’s possible for everyone to buy bread is if it costs $5. In the end, the same amount of bread would cost half as many dollars, meaning the amount you can purchase with a dollar, the value of the dollar, has doubled.

Keep in mind the increase of people also means that companies need to pay employees less. If the bread company employed the whole population and is selling 10 pieces of $10 bread, with $10 paid to employees to make the bread, then the only way for the company to stay in business when 20 people need food for $5 is to reduce employee pay to $5.

So this means that, in this scenario, you get paid less for every new person born. Moreover, the money you hold becomes more valuable every day, which means there’s a compelling reason to hold onto your money instead of purchasing bread (if you can hold out). This in turn means the bread company makes less money and thus might not be able to pay its employees.

This hypothetical example made a lot of simplifying assumptions. These assumptions are used to argue that a system in which no money is created has core flaws, flaws that risk people being unable to afford food. But these problems amplify rather than disappear when you start adding some of the complexities of the real world.

Factor in pay inequality, where any employee or business owner wants to be paid more than another (like if one person baked twice as much bread as everyone else).

Factor in the existence of multiple businesses or changing consumer demands (like if a noodle business competed with the bread business and convinced one bread customer to buy noodles instead, now the bread business can’t afford to pay all of its employees).

In this system where we factor in two real world conditions, people might not have the money they need in time to buy what they need. And to pay one person more than any other is to make it so that another person wouldn’t be able to afford food.

Overall this system is brittle. If any aspect of the economy doesn’t operate perfectly, then people end up with their needs not being met. The last time the US used this system was the gold standard, which multiple economists have argued prolonged or caused The Great Depression. Ultimately, the US was unable to end The Great Depression without partially transitioning away from the gold standard and leaving this kind of monetary system behind.

Option 2: Money is Actively Printed

Imagine if the government issued every newborn $100. In such a system money is constantly created, which means that many of the vulnerabilities of Option 1 would be resolved.

Prices wouldn’t have to decrease in order for everyone to afford food and consequently salaries wouldn’t have to decrease.

People could receive different levels of pay and, as long as enough money is created to satisfy the demand, nobody ends up unable to afford food.

Multiple businesses could be formed without necessitating that others fail since there are always new customers being born.

Having our government print money seems like it addresses the flaws of no new money being created, so what could go wrong? It turns out, history has a clear example.

Zimbabwe under Robert Mugabe used large amounts of government money to fund wars, to pay Mugabe, and to pay other corrupt officials. To afford this, the government printed money. This unbounded printing of money led the value of Zimbabwe’s currency to decrease. Why? In this case we would have the opposite situation as the example from Option 1. Rather than increasing people and fixed money, we have the amount of money increasing much faster than people, which means that bread will cost increasingly more dollars instead of less.

These actions, combined with widespread violence, poverty, and a rapidly declining business sector, resulted in foreign investors losing trust in Zimbabwe’s financial future. This fall in trust led the foreign investors to desire Zimbabwe’s money less and less. As a consequence, the value of Zimbabwe’s currency rapidly declined across the world. Robert Mugabe’s government responded to this by printing even more money.

The result?

At its worst point, the inflation rate reached 79,600,000,000% per month. An inflation rate that large would mean that, in the span of a month, a billionaire’s wealth becomes worth pennies. The average person’s wealth would require a microscope to see how small of a fraction of a penny their money is worth.

While creating money through simply printing it may have covered some of the weaknesses that Option 1 presented, it has a key weakness of its own. It requires whoever prints the money to print the right amount. Print too little and we end up back in Option 1. Print too much and we end up with Zimbabwe.

Option 3: Money is Created Through Debt

Another way to describe the shortcomings of the two previous options is a failure to sustainably satisfy supply and demand. How do you design a monetary system where enough money is supplied to those who demand it, addressing the pitfalls of Option 1, without allowing the unbounded demand that destroyed the supply in Option 2?

The current answer most governments use today: create an opposing force to any newly created money. Allow effectively unlimited money to be printed, but associate every new dollar printed with a cost. Essentially, instead of printing money, print debt. In this system, people can take on debt to increase their money in order to address the needs unmet in Option 1 while also being actively disincentivized against creating as much money as desired as in Option 2.

But this system is not without its own flaws and limitations. Most significantly:

How does the debt get paid back?

To answer this question, we first need to dig into the mechanics of how one creates money through debt.

How is Money Created Through Debt?

The way I described Option 3 might have made it sound like debt is created out of thin air, effectively the same as printing money. This is correct. Debt creates money out of thin air.

This concept is completely contrary to most of our daily experiences. If you lend a friend $20 and tell them to pay you back, nothing is being created out of thin air. The $20 comes from your pocket and goes into theirs; then when they have the money to afford it, $20 goes from their wallet back into yours.

But this is not how banks work. Banks don’t typically work with physical cash. They work with bank accounts which don’t follow the same rules as cash. The easiest way to explain is through example.

Commercial Banks

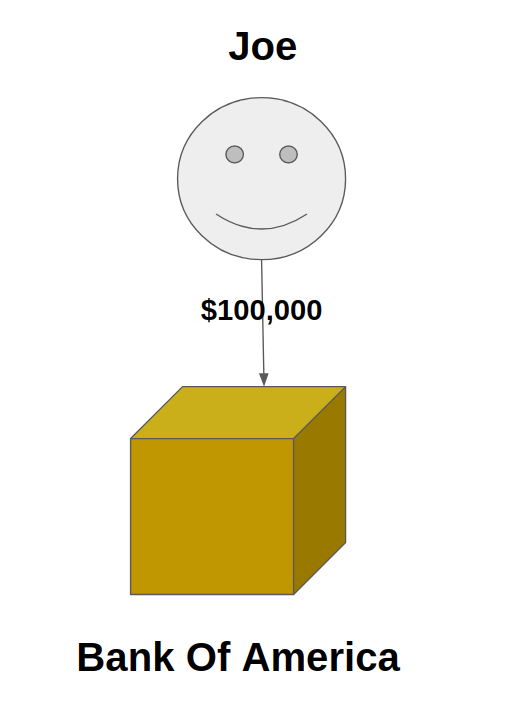

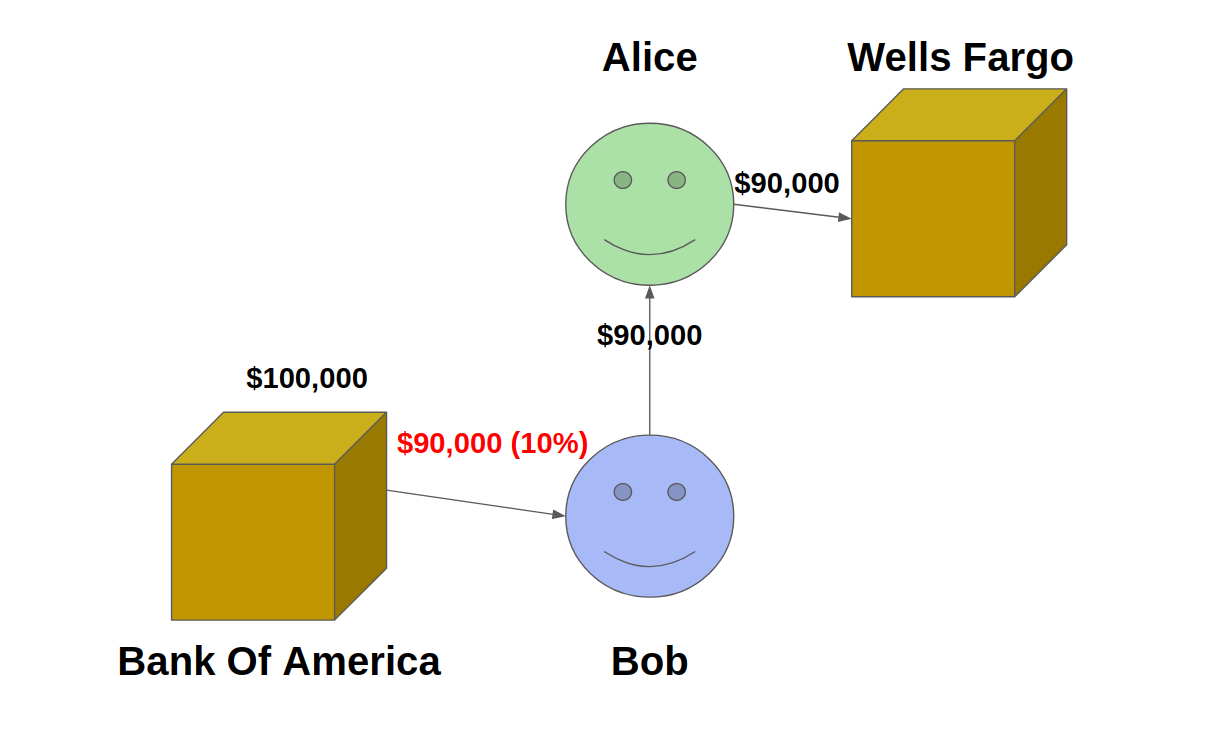

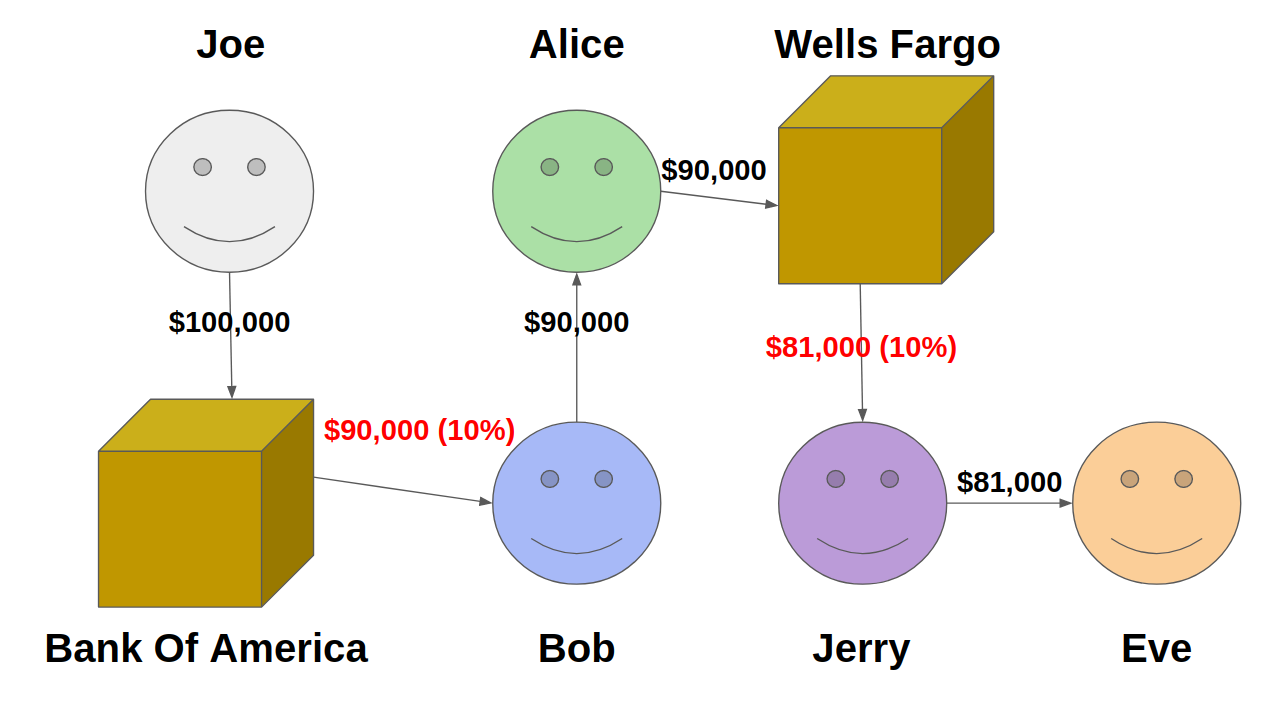

Commercial banks - like Bank of America or Wells Fargo - provide a service to the public. These banks offer accounts for you to deposit your money and offer loans to anyone needing money, like for mortgages. Banks are able to offer loans precisely because people deposit money into them, since they are legally allowed to loan out a fraction of their deposits. It is through combining these two services that commercial banks create money, as demonstrated below.

Even with no interest, we have created a system where more money was paid to the combination of Alice and Eve than Joe ever deposited, all without printing a single bill. Simply by allowing banks to loan out a fraction of the money that was given to them, money now exists to be spent that didn’t exist before.

However, if both Jerry and Bob are unable to pay their debts, then the banks don’t have the money to pay back Joe or Alice. If the debts aren’t able to be paid back, then Joe only has $10,000 and Alice only has $9,000 which, when you add these to Eve’s $81,000, gives you Joe’s original $100,000.

So you might think, sure $171,000 more was able to be spent, but no actual money was created. If people can’t pay their debt, the whole system collapses. This is where the Federal Reserve comes in.

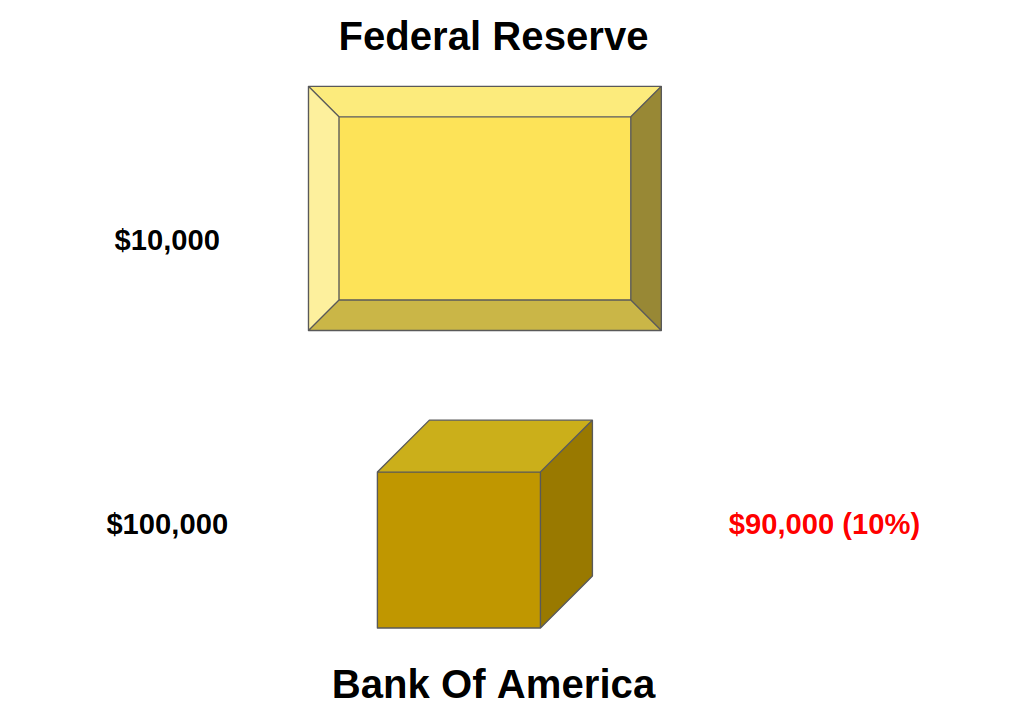

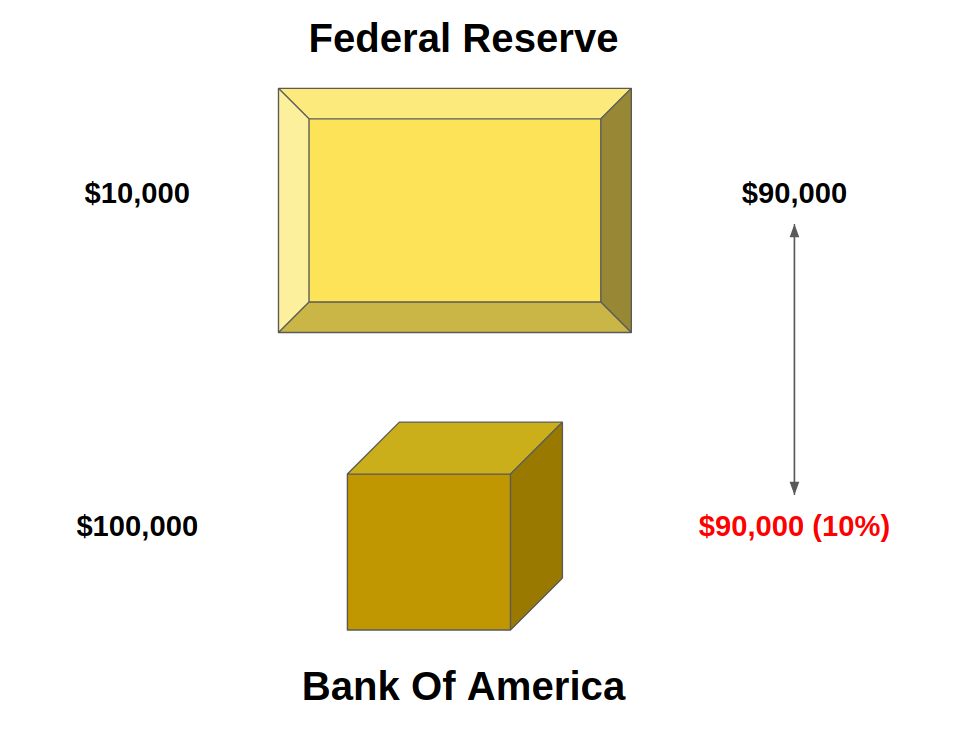

The Federal Reserve

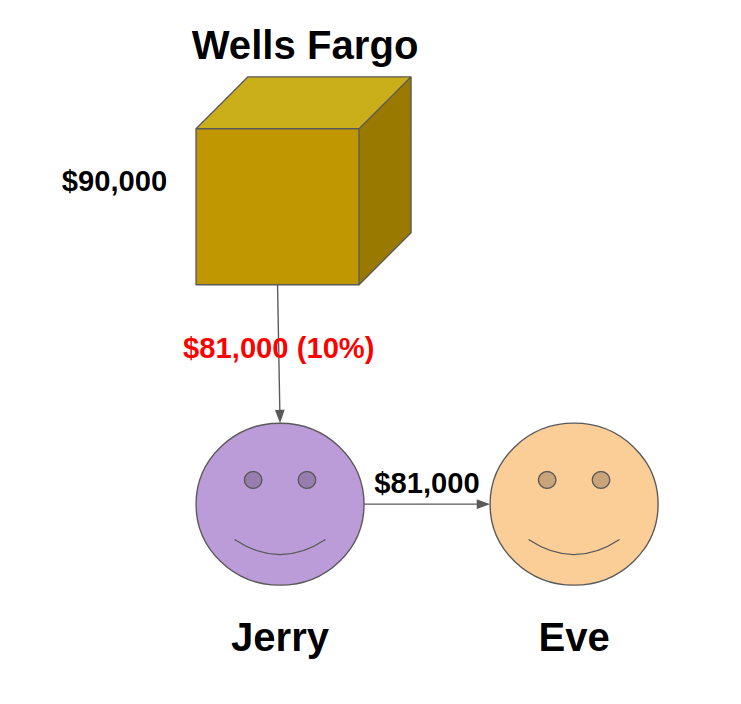

An individual cannot conduct business with the Federal Reserve. The Fed only conducts business with other banks, specifically by buying and selling loans. Through these actions of buying and selling, money is created in a way that no commercial bank can replicate, as the example below demonstrates.

You might think that Bank of America is out of luck in this situation. But that is incorrect. This is where money is truly created from scratch. The Fed buys Bob’s loan with $90,000 of newly created money, added to the Fed’s digital bank account with the click of a button.

This might seem like the Fed is simply printing money the same way Zimbabwe did. However, there is one key difference. Every dollar the Fed prints, every dollar they use to buy debt, the Fed is owed back that money plus interest. In this example, the Fed will receive 10% interest on their $90,000.

Even with these examples, questions still remain. How on earth is this sustainable? The only way everyone who assumes debt can pay it back is if new people take on debt. For the most part, that is correct. Rather than the government giving every child $100, this system assumes that there will always be new debt to cover old debt.

But there is another key way in which this increased amount of money created through debt stays in the system.

If Bob is unable to pay his loan of $90,000 while Bank of America still owns the debt, then Bank of America won’t have enough money to pay back Joe if he wants the entirety of the $100,00 that he deposited. If instead the Fed owns the debt and the debt isn’t repaid, then the Fed marks a failure to recoup the cost of the money it created, which is not necessarily detrimental to either the United States or the Fed.

To go into some technical detail, the Federal Reserve maintains a separate account from the US Treasury. This means that if the Fed loses money, the US Treasury does not lose money. The US Treasury is responsible for the money used for the National Government’s spending and thus manages paying the US debt. This debt is paid in part from taxes but also in part from the profits of the Federal Reserve. Whenever the Fed marks a loss, they simply stop paying profits to the Treasury until the loss is paid back, continuing to buy and sell debt in the meantime.

The ultimate effect of this system is that when debt is permanently unpaid, because of reasons like bankruptcy or cancellation of debt, the value of the debt permanently enters the economy.

If too much debt goes unpaid, the effect of the Fed's money creation transitions from creating money through debt to simply printing money. Should such a point be reached, you could expect similar backlash as occurred with Zimbabwe’s currency: a collapse in trust of the US dollar.

Most modern governments utilize a debt based system, effectively making the bet that future generations will continue to take on debt and, in cases where that debt can’t get paid back, faith in currency doesn’t collapse. Should this bet ever fail, it would not be unreasonable to assume that there will be another global financial reassessment of how money is created similar to when the last remnants of the gold standard fell with the end of the Bretton Woods system in the 1970s.

Conclusion

To explain the utilization of debt to create money, this article focused on a problem to be solved. “How do we create an economy that can sustain a growing population?” By focusing on this question and reconstructing the reasoning for utilizing a debt based economy, this article seeks to explain the cause of our current economic system. But the cause says nothing about the effect. More specifically, in our economy, when debt is the catalyst to generate money:

What happens to the money created by debt?

To be continued in part 2.

I find myself being edu-ma-cated by you, Jordan. Thank you!