The Future of the Video Game Market is Roblox

Why Roblox is poised to dominate the 2020s video game market like Nintendo did in the 2000s

Estimate Reading Time: 10 minutes

Prologue

When does technology drive the market?

As a child growing up with video games, I saw how games transformed from barely recognizable shapes moving around with a paper-thin plot into cinematic experiences rivaling Hollywood.

Witnessing this convinced me that the technology which mattered most for games was greater processing power and storage to better tell these types of stories. I was convinced advancements in those technologies would drive the growth of the video game market. And it has, to a small extent. But when you look at sales/revenue numbers, you see that a much larger chunk of the game industry is driven by different, much stronger factors.

After looking at the the data, I no longer believe that the future of the gaming market, which games rake in the most money, will be games that look like Hollywood films. Instead I am convince that the future of the gaming market is Roblox.

Why do I believe the future of gaming is a game that looks like Lego Island, a game created over 20 years ago? Answering the question requires me to tell the story of the past 20 years of the economics of video games.

The Rise of Casual Games (2000-2009)

At the turn of the millennium, the percentage of Americans who used the internet had only just broken 50%. Yahoo was still bigger than its competitor Google, who didn’t go public until 2004. Social Media was only just starting to form, with Myspace beginning in 2003. Smart phones were only just starting to be birthed, with the iPhone dropping in 2007.

And Nintendo dominated the video game market.

The Value of Accessibility

Going into the turn of the millennia, I looked forward to the advancement of games made for people who were deeply familiar with games. With that mindset, I fell in love with the technical promises of Sony and Microsoft’s consoles which were designed to appeal to gamers like me. When I saw that the Nintendo Wii would have across-the-board worse technical specs and thus be less capable of running the cinematic games I hungered for, I almost immediately dismissed the console, thinking it would flop.

And in the absence of my desire came the demand of hundreds of millions of others.

8 of the 10 top selling games of the 2000s were built for the Nintendo Wii. Five of these games were designed for an audience completely unfamiliar with video games, the so-called “casual gamer audience.” My fixation on what I believed made a “good game” led me, as well as Microsoft and Sony, to miss the real opportunity for innovation and greater sales. Not in stronger hardware that enabled games which appealed to existing gamers, but rather a completely different approach to controlling games that expanded the definition of the term “gamer.”

If you had never played a game before and then one day were told to control a young boy swinging a sword using this alien spaceship-looking piece of plastic, would you have any idea where to begin? It looks like you can press up or down in three different ways, there’s no button that says swing, and most people don’t have three hands so it’s not clear how you even begin to hold this spaceship.

Almost 30 million gamers did put themselves through this ordeal, but one can understand how this design creates a barrier to entry holding back non-gamers from picking up their first game. Contrast that controller design with the Nintendo Wii’s controller.

Almost everyone has at some point in their life either held a stick or a pool noodle and pretended to swing it like a sword. So if you were told to grab this white stick and swing it like a sword, you almost certainly have some intuition for how to do that. And that level of intuition is virtually all that you need to have fun playing the Nintendo Wii’s casual games.

By creating a controller and games that made gaming accessible to somebody who never played games before, Nintendo blew the gates to the gaming market wide open with the sales numbers to back it up.

Within the top 10 best selling games of 2000-20009, casual games sold 210M units while non-casual games designed for people familiar with games only sold 150M units. The implication of these numbers is that, through Nintendo’s market expansion, tens of millions of new gamers were born.

The Video Game Revenue Pie

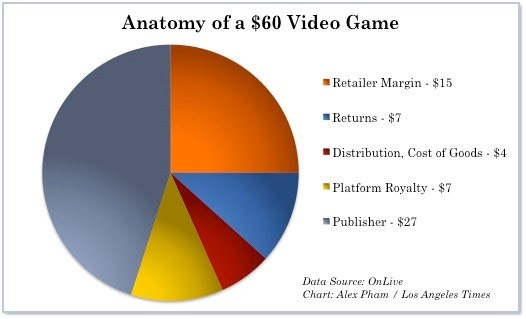

In the 2000s, video games were almost exclusively sold as physical copies. Physical games in physical stores that almost always ran on video game consoles. This led to a fairly defined breakdown within the market as to who made money in the video game industry and how.

Video game developers -11.6% of game sales - The people responsible for actually writing and building the game.

Video game console manufacturers - 11.6% of game sales - The companies behind the PlayStation and the Xbox, who made the hardware video games ran on. The hardware itself sometimes was sold at a loss, any game that was built on their hardware they took a fraction of that game’s sales.

Video game retailers - 25% of game sales - Companies like GameStop who held the copy of the game in their brick and mortar stores for customers to purchase. They typically made 25%.

Video game publishers - 45% of game sales - Investor, marketer, license manager and negotiator all in one. The publishers were the most financially invested in the games’ success and accordingly made the largest slice of the pie.

Nintendo was developer, console manufacturer, and publisher all in one, capturing 68% of sales from every one of their games sold. Combining this majority capture of sales with their domination of top selling games made Nintendo the dominant player of the 2000s.

The Rise of Free to Play (2010-2019)

League of Legends is a free game. It costs no money to start playing and you never are required to spend money. Despite that, in one decade, League of Legends made more money than Nintendo did from their 210M casual games sales that dominated the top 10 games of the prior decade.

In the decade following Nintendo’s domination, the technological landscape had changed drastically. Smartphones usage in America began the 2010s at 35% and ended it at 80% while internet usage in America reached almost 90%.

One might infer, given what drove the previous decade’s market leader, that these technological innovations would help make video games even more accessible and thus lead to more money made from an expanded gaming market. Which did indeed happen. Before smartphones, if you wanted to play a video game, you would need to sit in front of a computer or TV to do so. Now, you can pull out your smartphone while on a bus, in the bathroom, or at a restaurant and play a game.

However, this increase in accessibility fails to capture how a “free” game can make more money than a decade of paid games.

Digital Payments, the Lynchpin

Before the internet, a game company’s financial relationship with you began and ended with the sale of a game. But when the internet became standard, video game companies moved into your house, into your pocket. With the new ability for digital purchases to occur in a manner of seconds, now game companies could get money from you whenever you’re online.

An early strategy was subscription payments, where you pay a monthly or yearly fee to maintain access to the game. This is what we expect from services like Netflix, and the game World of Warcraft is well known for this model. But it’s the continual in-game purchases that make the most money. It’s the continual individual purchases that transform video games into at best, an online retailer, and at worst, a casino.

Why? A common argument is the ability for online games to take advantage of human psychological weaknesses. An oft-touted example is loot boxes, digital items in video games that you can spend real world money on to randomly receive a reward that may or may not improve your gameplay experience. This gaming mechanism was outlawed in Belgium as criminal gambling, yet globally is considered to be a $50B market.

Another exploitation of human psychology can be found in Candy Crush, which takes advantage of something called Hedonic Adaptation. Candy Crush is free, but there are in game limitations that prevent you from paying indefinitely for free. This restriction from being able to play the game pushes us to want to play the game more than if there were no restriction. And it’s here, facing this restriction and enhanced desire, that Candy Crush says “pay us money and we’ll give you what you want.”

Despite monetization strategies like this only resulting in 0.5-6% of a game’s userbase paying, that amount is enough to dwarf the revenues of the previous decade. That’s because, instead of one time payments of $60, the users who spend money on free games can pay multiple orders of magnitudes more, with one Candy Crush user spending $2600 in one day.

The internet had been around for decades. PayPal had been facilitating online payments since 1998. But the sheer rate of adoption of this long-standing technology means that 2010s’ video game market growth was driven not by technological innovation, but rather technological adoption. This adoption enabled free-to-play games to come into existence and dominate to the point that, just like how Nintendo swept 8 of the top 10 best selling games of the 2000s, free-to-play games swept 8 of the top 10 grossing games of the 2010s.

The Rise of The Engine (2020-)

20 years ago, less than 0.5% of the US workforce were programmers. Now, almost 3% are. Over that same time period, games grew from hundreds of Megabytes in size to almost three orders of magnitude larger. Behind the scenes of the game industry, much more is required of games than ever before and yet only 0.16% of all programmers are game developers.

Herein lies opportunity. A sizable increase of game complexity and requirements combined with a large number of potential game developers that are yet untapped begs for a solution that makes game development more accessible. And that solution the market begged for?

The game engine.

The Dark Horse of Game Monetization

What is a game engine? To put it succinctly, an engine is a set of building blocks one can use to make a video game. Imagine you wanted to build a new home. Would you rather chop all of the wood, build your own appliances, and make your own furniture, or go to Home Depot and Ikea for all of the building blocks and focus on the design? Game engines are the Home Depot/Ikea of video games.

Game engines have been around for decades. One of the biggest and the oldest, the Unreal Engine, was first showcased in 1998. However, they didn’t always hold the same importance as they do now. For a while it was manageable to build your own games from scratch. With a dog house, you could afford to cut your own wood and build everything on your own. With the high rise luxury condos that many have come to expect of many modern games? You need an engine.

This now adds a new contender to the game revenue pie. While a game developer might make 11.6% of sales and a game publisher might make 45% of sales during the 2000s, using a game engine like the Unreal Engine will take a 5% slice before either of those two can get their cut.

But why settle for a slice when you can have the whole pie?

Nintendo, back in the early 2000s, was able to eat almost 70% of the pie of games they made because they were the developers/publisher of the games and owned the consoles. However, they lacked a significant retail store presence, preventing 100% revenue capture.

Epic Games, the creator of the Unreal Engine, has no such issues. With their digital game store they capture the revenue share of their own games that Nintendo missed. But on top of that, because they own both the store and the engine, they are able to capture almost twice the revenue slice from the games of other developers (who use their stores and engine) than Nintendo did with games built for their consoles.

This domination of game production helps explain why Epic Games made hundreds of millions of dollars in 2020 while their closest competitor in the engine space, Unity, lost hundreds of millions of dollars. However, I would still claim that despite all of this, they remain the present and not the future.

Epic Games dominates the market as it currently stands, but they aren’t doing enough to expand the market.

The Future of Engines

Through one lens Roblox and Epic Games are nearly identical. They both provide a game engine for themselves and others to develop games with and they both provide a platform to buy and sell games. But their crucial difference lies in branding.

Epic Games’ Unreal Engine is known as a game engine. Roblox is known as a game. This subtle difference means that Roblox attracts the video game playing audience as opposed to just the video game developer audience. Then, they present to the 150 million people playing Roblox the possibility of making games and money from those games using Roblox’s engine. The result? 7 million developers making over $200M. 4.7% of Roblox players have become game developers compared to the 0.16% of programmers who have become game developers.

The unassuming art style shown in the intro works in Roblox’s favor for this purpose. For people who’ve never considered making a game before, what feels more approachable, making a game that looks like the image on the left (Roblox) or the image on the right (Unreal Engine)?

Technology drives the market only when technology enables more money to be made. Timing, adoption, and branding sold more in the past two decades than the latest tech. Roblox will not define the future because it’s technology is future defining. It will be the future of game engines, of games, because by branding itself as a game first and maintaining an approachable aesthetic, Roblox is expanding the market of game developers the same way Nintendo expanded the market of game players.